Catch-Up / Rescue Bookkeeping – A Case Study

While every bookkeeping job comes with its own set of unique tasks, clients seeking catch-up (or Rescue Bookkeeping) tend to bring with them a host of relatively predictable (if dynamic) issues that you can manage effectively if you are aware of them.

A typical catch-up bookkeeping scenario

Recently we were contacted by the operator of a sole trader business – “Peter” (not his real name), seeking help with his bookkeeping backlog.

Many of the issues he identified are relatively standard in the rescue bookkeeping world. Becoming familiar with them will help you to effectively help your clients in the future.

Tax returns in arrears

By definition, anyone seeking help with catch-up bookkeeping will have a backlog of some kind.

By definition, anyone seeking help with catch-up bookkeeping will have a backlog of some kind.

In Peter’s case, he is three years behind with his tax returns.

With catch-up bookkeeping, there is a high likelihood that your client’s systems for maintaining their receipts are inadequate, and that there will be missing receipts and records. The further back the backlog reaches, the more information gaps you will encounter, while reconciliations become more time consuming.

This case study is an ideal example of what someone should understand if they are perform online Customer Service work or if you are a contract bookkeeper.

Business and personal bookkeeping records

Like most people seeking rescue bookkeeping, Peter’s business and personal transactions have not been separated. In addition to operating a sole trader business, he takes on casual work in Aged and Disability Care in a personal capacity, so his statements contain transactions that relate to (but don’t differentiate between) each of these roles.

Peter’s QuickBooks Online account also only has the registration details of his sole trader business, so he is unsure how to enter and deal with the casual contracts that he undertakes in the Aged and Disability sector.

Peter’s QuickBooks Online account also only has the registration details of his sole trader business, so he is unsure how to enter and deal with the casual contracts that he undertakes in the Aged and Disability sector.

Peter has also a recently purchased an investment property. So, between his casual work, his sole trader business and the recently purchased investment property, he has several distinct income streams and transaction which will complicate reconciliation and data entry tasks.

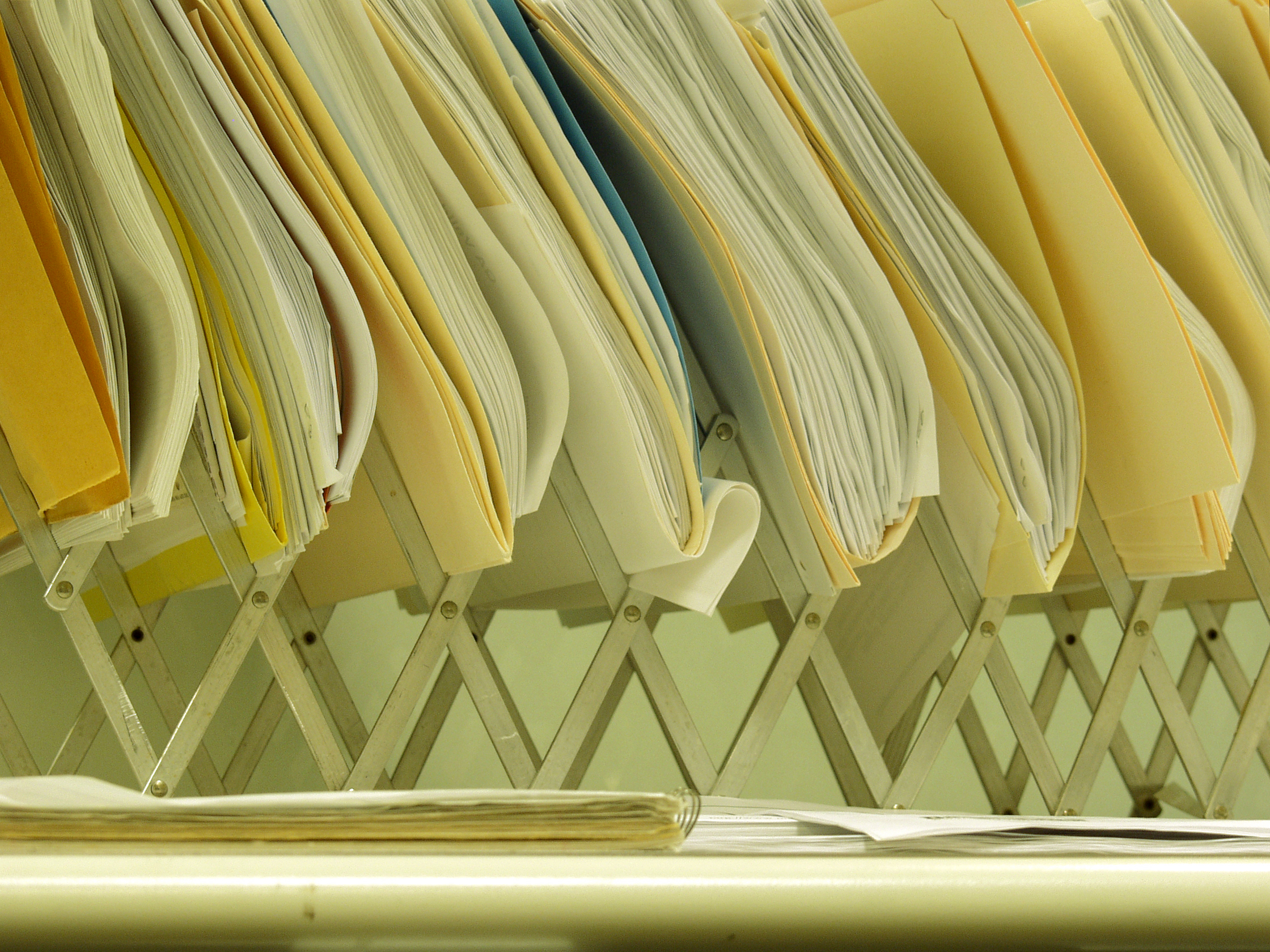

Tax receipts

Peter doesn’t make huge amounts of transactions, but because he is three years behind, he has accumulated 200 receipts.

This is a significant data entry burden, and given the extended timeframe, it is safe to assume that not all receipts will be retrievable, and that there will be discrepancies. Some receipts may also have gone white and can’t be read if they are exposed to sunlight!

Peter’s receipts are in hard copy (he doesn’t use Hubdoc or other Receipt Capture software that would enable him to create and keep a digital record), and his bank does not enable him to use bank feeds to import transactions onto QuickBooks.

Peter’s receipts are in hard copy (he doesn’t use Hubdoc or other Receipt Capture software that would enable him to create and keep a digital record), and his bank does not enable him to use bank feeds to import transactions onto QuickBooks.

In this case you will need to problem solve a solution, to avoid a scenario where the client physically posts the receipts to you, which risks resulting in a range of negative outcomes for you and for them, if the receipts are lost prior to creating a digital record.

Attention of the ATO

Peter is concerned that because the majority of his transactions are business expenses, and because he expects a sizable return, that he will be a “red flag” for ATO auditors.

He has been informed that the ATO are reasonably easy to deal with as long as he communicates regularly and give them an update of the work that has been completed and when he expects to complete it all.

Be ready to discuss with your client issues around dealing with the ATO

For this reason, he is concerned about how to deal with the ATO, and he wants to be armed with all the information he needs prior to lodging.

Income and expenses

In many cases, catch-up bookkeeping clients won’t have attended to any record keeping at all.

In Peter’s case, he has been on top of some income records, but has neglected his expenses.

While Peter is confident that expenses will exceed revenue, and that he is due a refund, because he has neglected recordkeeping tasks, there is no guarantee that his perception is accurate, or that he is completely clear on the financial state of his business. For this reason, he needs to be prepared for any unwanted surprises.

Communicating about Receipts and Expenses

One of the unexpected costs associated with Rescue Bookkeeping is the time it takes. You may come across some receipts and need confirmation of the account code to use (or to know if it is personal or business) and Peter might not know right away.

Peter might also be very busy earning an income that he is not able to return your call/email/sms until the end of the day – or, 2 weeks later!

This time lag can end up becoming VERY frustrating and may require you to be MORE efficient in your coding and messages.

Avoiding costs

Peter is very keen to keep expenses down, which is one of the reasons he has never engaged the services of a BAS agent or an accountant, and in fact one of the reasons he is now seeking rescue bookkeeping.

There may be some tasks that relate to Tax/GST that can only be performed by a Registered BAS Agent or under guidance from the owner or business accountant.

Peter saw the Level 1 Bookkeeper Rates and wanted to pay those rates but he may also need help from someone more experienced.

In these circumstances it is important to keep in mind the parameters of the job, and to ensure that you do not mistakenly agree to any work that might be out of your skillset or capability.

Certificate in Xero, MYOB or QuickBooks Online

One of the cheapest ways to upskill and learn how to use Xero and MYOB to perform daily transactions and bank reconciliation tasks is to enrol into a Premium Short Course or MYOB & Xero Certificate Course Package.

You’ll learn how to use these accounting programs to perform these tasks yourself or be a better manager if you get a contract bookkeeper to do the work for you.